To read the supporting article by Moritz: click here

This episode is not for everyone. It doesn’t include chatting about how to read charts, pick stock directions, or even manage your trading mentality.

But for some, this episode will turn heads and bend preconceived notions about the deal. We spotlight what happens when we discover structural inefficiencies that can be exploited, as was the case with today’s guest Moritz Seibert.

Many know Moritz as a trend following guy and a vested interest in the crypto markets, but (mostly) know that he used to arbitrage warrants on the German DAX. No one. It’s an extreme edge and he traded it hard for three years.

Moritz has never spoken publicly about arbitrage before! In the course of this summary, he details all aspects: markets, inefficiencies, trade, and the inevitable decline.

Disclaimer

Trading in financial markets involves the risk of loss. Podcast episodes and other content produced by Chat With Traders are for informational or educational purposes only and do not constitute trading or investment recommendations or advice.

Topic and Timestamp

Note: Exact time depends on current ad.

- 03:10 – Market: Warrants, the nuances of structured retail products.

- 16:10 – Inefficiency: Finding an exploitable edge, why it exists.

- 28:10 – Trading: paper trading, technology and structured positions.

- 46:50 – Decline: Counterparty Tricks, Next “After Hours” Deal.

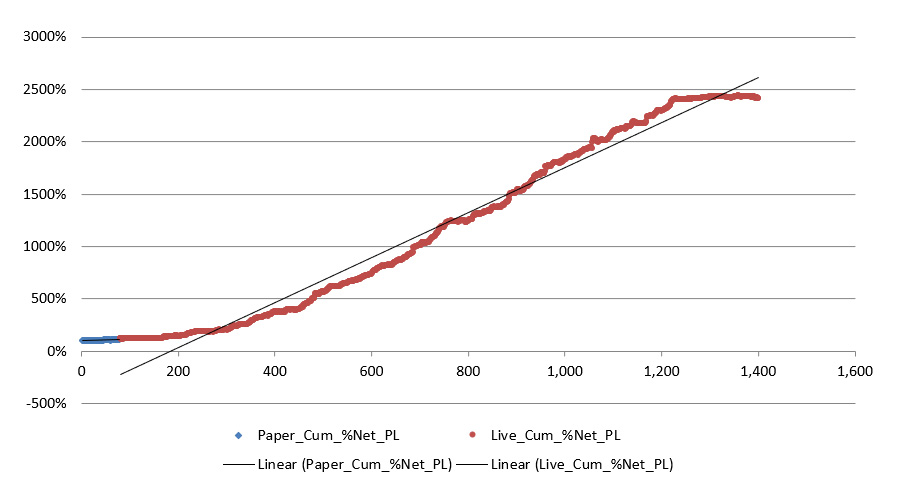

Strategy Performance: Equity Curve.

Strategy Performance: Spread Distribution.

additional comment

From Moritz:

Spread distribution is a way of normalizing trading results. Just as trend followers tend to measure trade results in terms of R, N, or ATR (e.g. this trade made 7 ATR and this trade lost 0.5 ATR), my PnL is spread It can be displayed conditionally. Spread is the bid/offer (B/O) spread observed on the warrant at the opening of the trade.

One of the reasons the trades worked was that the spreads offered by banks were usually too low, at 1 cent. The total cost of the B/O spread was 2 cents, as both calls and puts had to be traded. Once you have exited the trade with either a profit or a loss, you can put this PnL back into your spread terms to normalize your results over time.

Let’s say you trade 10K calls and 12K puts. The total B/O cost was $100 (1 cent * 10K) for the call and $120 (1 cent * 12K) for the put. Now, let’s say that this trade resulted in a loss of $440. PnL in spread conditions is doubled (440/220). This allows us to view PnL regardless of deal size and better analyze the quality of a typical trading approach.