This is the central tenant of how options are priced, and it is often the traders with the most accurate volatility forecasts who win in the long run.

Whether we like it or not, we take an intrinsic view of volatility whenever we buy or sell options. Buying options means that volatility (or how much the options market thinks the underlying asset will move before expiration) is cheap, and vice versa.

Based on volatility, some traders have given up completely predicting price direction, preferring instead to trade based on volatility ups and downs in a market-neutral manner.

Some options spreads use the building blocks of volatility trading, strangles and straddles, to enable such market-neutral trading.

But even though straddles and strangles are the norm, they can sometimes leave something out for traders who want to express a more nuanced view of the market or limit their exposure.

This is why spreads like the Iron Condor and Butterfly exist, allowing traders to change their risk parameters to bet on changes in options market volatility.

Today we will discuss one of the most misunderstood option spreads, the Iron Condor, and the situations in which traders want to use it in favor of short strangles.

What is short strangle?

Before we delve into the details of the iron condor and what makes it tick, Short Strangle is a short volatility strategy that many consider to be the building block of the Iron Condor. Since iron condors are essentially short strangles that are hedged, they are worth understanding.

A strangle consists of an out-of-the-money put and an OTM call, both within the same expiry date. In Longstrangle these he buys two options and in Shortstrangle he sells them. The purpose of trading is to bet on changes in volatility without knowing the full price direction.

As mentioned earlier, strangles and straddles are the building blocks of option volatility trading. More complex spreads are built using a combination of strangles, straddles and “wings”. This will be explained later in the article.

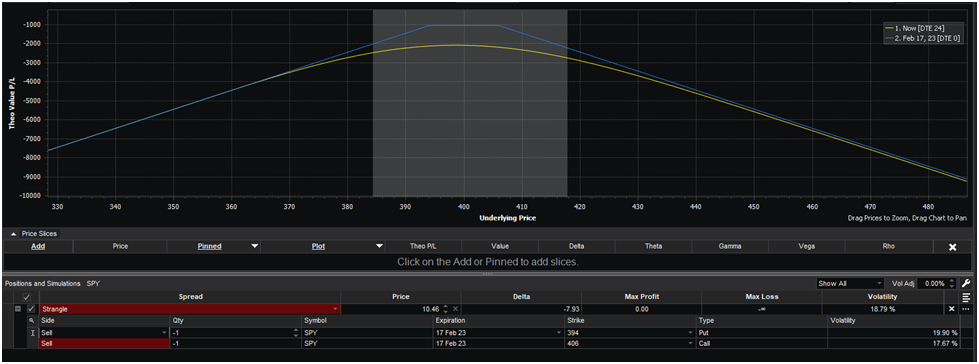

This is an example of a textbook short strangler.

The goal of this trade is for the underlying to trade within the 395-405 range. If this happens, both options expire and you pocket the entire credit you collected when you opened the trade.

However, as you can see, when the market moves outside the shaded gray area, losses start to mount. You can easily calculate your break-even level by adding transaction credit to each strike.

In this case, you received $10.46 to open this trade, so your breakeven levels are 415.46 and 384.54.

However, a potential problem arises here. As you can see, the potential loss on this trade is undefined. If the underlying stuff gets messed up, you never know where it will be by the expiration date.

For this reason, some traders look to spreads like iron condors that allow them to bet on volatility in a market-neutral manner while defining the maximum risk of a trade.

The iron condor has a “winged” strangler

The Iron Condor is an excellent choice for traders who don’t have the temperament or the luxury to sell straddles and strangles.

The spread consists of 4 contracts. 2 calls and 2 puts. For simplicity, let’s make a hypothesis. The underlying SPY is 400. Perhaps you think the implied volatility is too high and want to sell some options to take advantage of it.

We can start by building a 0.30 delta straddle on this underlying asset. Let’s use the same example: sell 412 calls and 388 puts. You will see the same payoff diagram as above. I love collecting big premiums, but I don’t like that undefined risk.

What’s the easiest way to mitigate this straddle risk without labeling anything? Both puts and calls are more out of the money than our straddle. It’s that simple. You can purchase more out-of-the-money options. This is the iron condor, astride the “wings”.

Another way to look at the Iron Condor is to build two vertical credit spreads. After all, halving the iron condor payoff diagram equals the vertical spread.

With an underlying asset price of 400, a standard iron condor looks like this:

● Buy 375 Put

● sell 388 put

● sell 412 call

● BUY 425 call

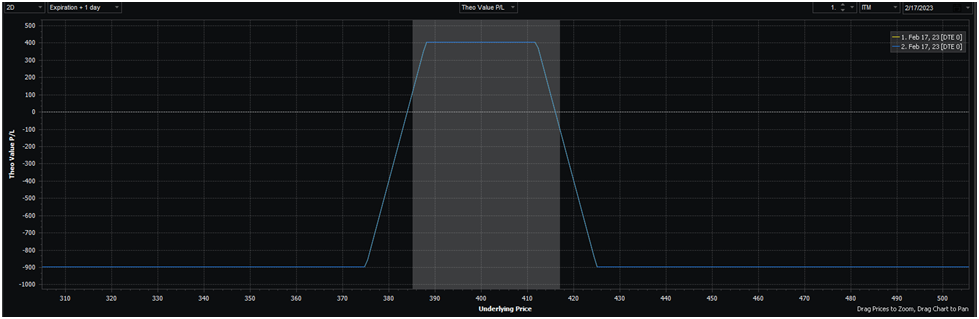

The payoff diagram looks like this:

Determining Use of Iron Condor vs. Short Strangle

Have you ever wondered why the majority of professional options traders tend to be net sellers of options?

Many natural customers in the options market use them to hedge against portfolio declines, whether they buy puts or calls.

Much like Florida homeowners buy hurricane insurance, they essentially use options as a form of insurance. by a hurricane.

Many option buyers (but not all!) work similarly. They bought puts on the S&P 500 to protect their stock portfolios and hope the puts are worthless, just as Florida homeowners are praying they never really have to. . use their hurricane insurance.

This behavioral bias in options markets results from a market anomaly known as the volatility risk premium. This means that implied volatility tends to be higher than realized volatility. Therefore, net sellers of options can trade strategically and take advantage of this anomaly to profit.

However, there is a caveat. The revenue streams that exist have some drawbacks, perhaps a less than ideal revenue profile in exchange for earning above the benchmark. If there is a sell option, the risk profile scares people away from harvesting those returns.

As you know, selling options carries theoretically unlimited risk. When selling a call, it is important to remember that you are selling someone else the right to buy the underlying stock at the strike price. Stocks can go up indefinitely, and no matter how high the stock goes, you’re on the hook to fill your side of the trade.

So while there may be positive expected value methods to trade from the short side, many are unwilling to take that huge and undefined risk.

This is where spreads like the Iron Condor come into play. Additional out-of-the-money puts and calls, often referred to as ‘wings’, can help contain losses and short volatility without the potential for catastrophe.

But it’s not a free lunch. By buying these two his OTM options, you are sacrificing your profit potential to be safe from catastrophic losses. And for many traders, this is too high a cost to harvest his VRP.

In almost any backtest or simulation, Hedging is generally -EV, so the short strangle is the clear winner. For example, take this his CBOE index, which tracks the performance of his one-month .15/.05 Delta Iron Condor portfolio on his SPX since 1986.

In addition, there are commission considerations. Iron Condor consists of 4 contracts, 2 puts and 2 calls. This means that iron condors charge twice as much as short strangles in most options trading fee models.

With entry-rate retail options trading fees hovering at around $0.60 per contract, it costs $4.80 to open and close the Iron Condor.

This is a significant stumbling block as most iron condors have fairly low max profit and commissions are often over 5% of max profit and have a large impact on the final expected value.

Ultimately it comes at a cost in terms of expected value and additional fees for placing the iron condor. Therefore, you need a compelling reason to replace the iron condor in favor of short strangles.

Conclusion

Too many traders get stuck in the “I am an iron condor income trader” mentality. Markets are too chaotic and dynamic to take such a static approach. The reality is that any given underlying has an ideal strategy of risk tolerance at any given time.

Sometimes you want short volatility strategies across market regimes, and sometimes you want more nuanced approaches such as calendar spreads.

For example, it may make sense to trade iron condors when implied volatility is very high. Any short volume strategy is high enough to print money, but too high for a naked short option. Similarly, iron condors may be far from ideal trading spreads.

Related article