")

As we approach spring 2023, the US housing market is not crashing nationwide. far cry. Home prices fell the most in the same metropolitan areas that saw the biggest gains since 2020.

according to NewsweekHere are the cities where house prices have fallen significantly so far:

- Austin, Texas

- San Francisco, California

- San Diego, California

- Phoenix, Arizona

- Denver, Colorado

- Seattle, Washington

- Tampa, Florida

Home prices in Austin are expected to drop by more than 15% next year, while San Francisco, San Diego, Phoenix, Denver, Seattle and Tampa will see prices drop by more than 10% in 2023.

Home prices fell just 0.1% in January 2023, with a typical home price of $329,542, 4.1% below the peak set in July 2022, according to the Zillow Home Value Index. . Home prices are up 6.2% year-on-year, decelerating sharply from a near-record 18.8% year-on-year growth in April. Zillow predicts that typical U.S. home prices will rise 0.5% from January 2023 to January 2024 (seasonally adjusted).[1]

There is some evidence to suggest that we are on the verge of the worst housing meltdown in recent American history, but current pricing statistics show no significant change. Based on the month’s collapse in buyer interest and falling listed home prices, there are growing signs that this is the beginning of another housing recession similar to the one seen in 2008. This article explores the disturbing details of the 2023 housing crash, its causes and implications for the future.

2020-2022 housing boom

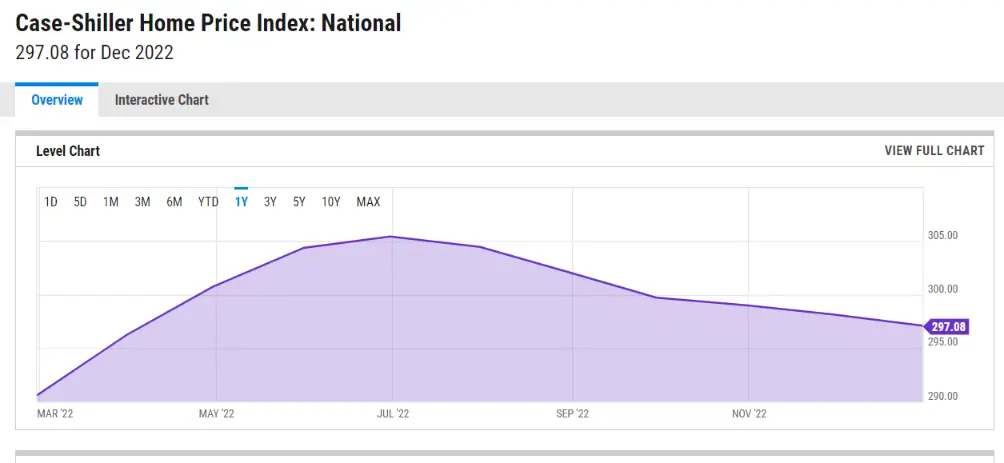

From March 2020 to June 2022, median home prices, as measured by the Case Shiller Index, increased 43%. This incredible ascent was never thought possible. Real estate investors and homeowners have millions of dollars in cash in this era of hyper-growth, with owners drawing record stocks through his HELOCs and buyers watching prices rise month by month. I was desperate to see it. During the peak of the housing market in 2021-2022, homebuyers were embroiled in a bidding war, even buying homes they had never seen in person. After 27 months of near-parabolic growth, the market stopped rising at a runaway pace in June 2022. The economic impact of higher Fed rates and inflation on homebuyers has put a stop to the rapid rise in home prices in 2022.

2023 Housing Crash

The trends in the housing market are finally starting to change. It was the fifth month in a row of declines, down 3.6% from its peak. To many, this seems a slight diminution compared to what happened three years before him. Case-Shiller would need to drop another 28% for prices to drop to pre-pandemic levels. The 3.6% decline is largely unnoticed by buyers, but there is growing evidence that this is the beginning of another housing market collapse similar to the one seen in 2008. From the base value of historic home prices and the alternative value of new homes. Multi-million dollar starter home prices in big cities are not sustainable in an economy with runaway inflation, high energy costs and a cost of living crisis.

Evidence of a 2023 housing crash

Evidence of a 2023 housing crash can be found in shocking new weekly data. For example, Case Shiller’s latest release revealed that the price has been dropping for six months. This may not seem like a big deal, but history shows that this decline happens infrequently. In fact, since 1986, Case-Shiller’s first reading, the market has rarely fallen more than his 3%. The only exception is the decline of only 3.05% in 2008 and 1990.

Many experts speculate that we are in the crash denial phase. There are many people who refuse to compromise on price and are private sellers who maintain this illusion of the market. Home sellers cling to past highs rather than comparing to the price they paid for their home. I have a cognitive bias that As frustrating as it may be for buyers, previous crashes have shown that individual sellers are not the first home sellers to move in any real estate market. They are almost always the last to sell because of the real estate agent’s costs and the costs of buying and moving into a new home. If , you are a builder. Builders look at market demand for land costs, license fees, material costs, labor costs, and geographic location. They set costs for profit margins and do not entrench a cognitive bias for what they pay. Builders want to create and move inventory for profit.

The role of builders in the 2023 housing crash

Builders are multi-billion dollar companies that move thousands of units each month and have entire teams dedicated to pricing. There is a much higher incentive to lower prices to move inventory. In this quarter, nearly all serious builders lowered prices and incorporated incentives such as price buy-downs to get people to buy. So while Case Shiller’s graph looks fine so far, it doesn’t really tell you what’s going on. The latest earnings report from the builder reveals some serious market issues.

Meaning for the future

It will take some time for the effects of these actions to be reflected in the existing housing market, but there is no denying that these developments in new residential spaces will have an impact. Imagine you’re buying an existing home, and the new home on the street suddenly cuts its price by 20%, making it on par with the existing home you’re looking at. There’s always a premium between stocks, so it’s almost certain to sway your buying decision. A new home always locks the price into the cost of the purchase.

The evidence for the slowdown in new homes is pretty simple, but not all gains in 2020 and beyond will suddenly disappear overnight. The housing market is at a crossroads. For generations, owning a home has been part of the American dream, and that dream is threatened by a simple calculation.

affordable housing

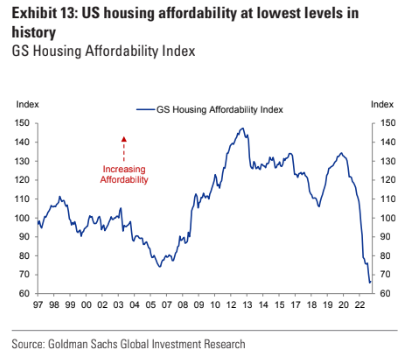

To demonstrate this fact, we can look at the affordability of housing. Using data from the U.S. Census Bureau, the Fed, and the U.S. Department of Housing, the American who bought the median home in 2022 is currently paying more than 52% of his pre-tax gross income on a mortgage. I understand. We are now well above 2008 relative prices, and if this is the worst real estate bubble the country has ever seen, then we have to ask ourselves what is different about this real estate bubble.

US housing affordability is at an all-time low.

One of the three variables we have to offer is price, and looking at affordable charts, it’s easy to see why so many people are asking for a crash. Unemployment is near record lows and home ownership is out of reach despite very good incomes over the past five years. Without demand from ordinary Americans, it becomes increasingly difficult to keep supply low. As stock availability becomes apparent, prices will drop as demand must meet supply at the appropriate price level.

Conclusion

In conclusion, while the housing market has not yet crashed, there is growing evidence that it is on the brink of the worst housing meltdown in recent American history. The proof can be found in the shocking new data updated every week. Builders are multi-billion dollar companies that move thousands of units each month and have entire teams dedicated to pricing. There is a much higher incentive to lower prices to move inventory.

Undoubtedly, these developments in new residential spaces will impact the existing housing market.The latest earnings reports from builders reveal some serious market issues. Without demand from everyday Americans, it becomes increasingly difficult to keep supply low. Lowering both new and existing home prices is the first signal of increased supply to buyer demand at those price levels. Displaced home sellers will give up when inventory becomes clear. The market is at a crossroads and could enter a long and painful bear market next year.