")

last thursday headline He told us that Germany, the world’s fourth largest economy, was in recession. German consumers suffered months of high inflation and lost their livelihoods.

up to date data It shows that the country’s inflation rate has fallen to 7.2%. Both food and electricity prices are more than 15% higher than they were a year ago. This is a sharp reversal for a country whose inflation averaged around 1% for more than 20 years before starting to accelerate in January 2021.

The reasons for the recession were obvious, but in retrospect, students of history will wonder how the era was defined. Germany is in recession after suffering two consecutive quarters of declining GDP.

Here in the United States, there has never been a clearer consensus on the question of what causes a recession. In fact, the debate over the precise definition of recession didn’t occur to him less than a year ago.

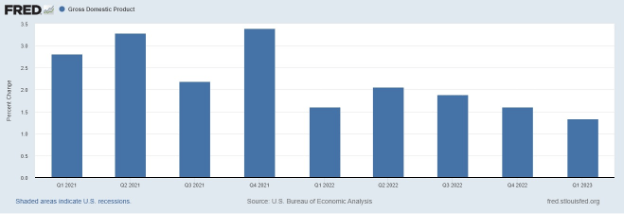

July 2022, NPR Asked If the economy slips into recession after two straight quarters of contraction. Initial forecasts were for GDP to contract by 0.9% in Q2 2022 and 1.6% in Q1.

White House officials, including President Biden, claimed that it was not in recession. They pointed to other economic indicators that the economy continues to grow.

Nearly a year later, we know those officials were right. The two-quarter decline was not evidence of a recession.

sauce: federal reserve

What we learned from last year’s discussion is that a recession looks like this: defined It is evaluated by several metrics, as outlined below.

- Real personal income less transfers.

- Salary employment in the non-agricultural sector.

- Real personal consumption expenditure.

- Wholesale and retail sales adjusted for price changes.

- Employment as measured by household surveys.

- industrial production.

The National Economic Research Service says there are “no set rules about what indicators inform the process or how they weigh in decisions.”

Most of these metrics are at or near all-time highs and trending upward. This is why economists say we are not in recession.

The problem, however, is that the index could reach all-time highs once the recession sets in. In fact, it often does.

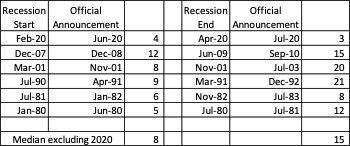

Economists look for weakness in indicators to determine when a recession has started. That means decisions are always made after a recession has set in. On average, official announcements come eight months after the recession begins.

Note that the table below excludes the 2020 recession as it is its own data point.

sauce: NBER

This means consumers have been feeling the pain of the recession for months. Before Economists and policy makers also agree with them that pain is real. Meanwhile, investors are also facing pain.

Ignoring the 2020 recession, stocks fell 4 out of 5 times between the start of the recession and the announcement. Bank stocks were among the hardest hit during the period, dropping an average of 13%. The worst drop was his 39% drop in 2008. The best case was his 6% recovery in 1980.

Banks will be particularly vulnerable during that period. The economy is shrinking. But the data don’t support it. This can lead bankers to make wrong decisions.

Banks act on data even when they know things could go wrong. This was famously summed up by Citigroup’s CEO in July 2007.

The recession had not yet begun, but the housing market was already in decline. So did stocks.

according to new york times, the former chief executive, infamously said in July 2007 (referring to the company’s leveraged lending practices): But as long as the music is playing, you have to get up and dance. we’re still dancing ”

He admitted that there would be problems. But that didn’t stop banks from having these problems. Doing so means sacrificing profits and potentially losing customers.

Banks are still dancing today. History teaches us that things get complicated. And they will get uglier.

That’s why Adam O’Dell and his team are so committed to this issue. After months of monitoring the financial bank situation, they know worse things are to come.

And they’ve found ways to help us prepare for what happens when the music ends and more bank busts follow.

Adam published his list yesterday 282 US Financial Stocks He thinks we should sell now… especially including the four that could go down next.

Of course, managing risk when inflation rises is not enough.

That’s why Adam also showed us how to make “non-Wall Street deals” for a handful of companies facing significant systemic risk for a chance to build wealth in the midst of a crisis.

All details including the 4 companies that may be holding your deposit, here i am.

nice to meet you, Michael KerrEditor, one trade

Michael KerrEditor, one trade

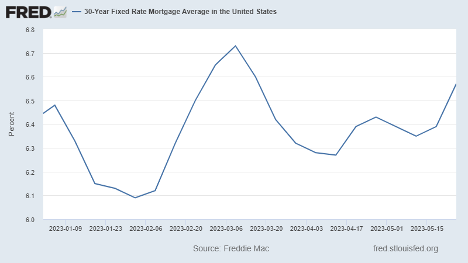

In the midst of the debt ceiling drama, you may have missed it, but U.S. mortgage rates have been quietly rising in recent weeks. The 30-year average interest rate is currently 6.57%.

While still below the 7.1% recorded in November, interest rates have risen for most of this year, especially the last six weeks.

Higher interest rates make buying a home harder, especially for first-time buyers who may not have a lot of cash on hand for a down payment.

Example: A $500,000 home with a 3% mortgage of $450,000 would have monthly principal and interest payments of $1,897.

At the current interest rate of 6.57%, that same house would cost you $2,865. You’ll end up spending nearly $1,000 more on your mortgage alone.

But the damage to house prices has been minimal and may be over.

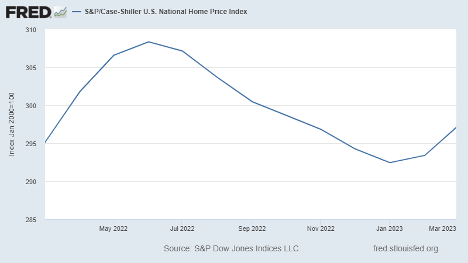

March Case-Shiller Home Price Index values released this week. And despite looking at data that is nearly two months old at the time of its release, the data can still show general trends. House prices rose in both February and March after a string of declines since June last year.

Certain parts of this country are really hurting.

San Francisco’s housing market, for example, has been hit hard by the rush of tech-related layoffs over the past year. Nationwide, however, home prices have remained roughly flat over the past year, falling only a modest 3.5% from their all-time highs.

Is the housing price decline over?

Ultimately, it may all come down to whether or not we finally get the recession we’ve been anticipating for a year.

However, given that supply remains very tight, we don’t expect prices to drop significantly…at least not any time soon.

nice to meet you,

Charles SizemoreEditor-in-chief, The Banyan Edge

Charles SizemoreEditor-in-chief, The Banyan Edge