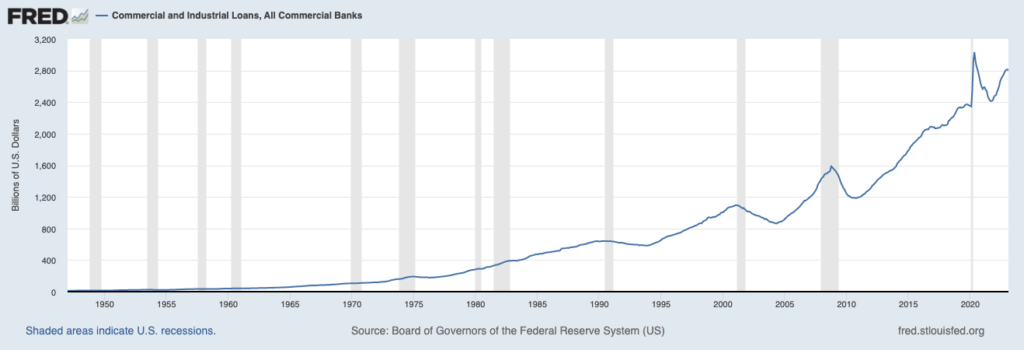

This is it. It’s the only chart you have to watch out for right now if you’re trying to figure out where the economy is headed. Construction and industrial (C&I) loans are a (roughly) $2.8 trillion business for banks nationwide. When they roll over, they make a soft landing. If they roll hard, it’s a hard landing. It’s not complicated. The only things hanging in the air are timing and severity.

C&I loans take the form of either lump sum payments or revolving credits. They can expand their businesses, hire people, invest in new equipment and facilities, improve property occupied by their owners, or obtain working capital, usually for a year or two in length. This is what small and midsize banks really do outside of mortgages and checking accounts. It’s their real business. It’s their whole purpose to exist. Small businesses cannot use Wall Street for capital. They cannot issue bonds or sell shares. They need the bank to grow, improve and fund new projects.

The economy also needs this activity. The SBA estimates that in the 20-year period from 2000 to 2019, he 64.9% of all new jobs were created by businesses with fewer than 500 employees. This represents two-thirds of total US job growth over the last 20 years, mostly financed by C&I loans and credit agreements between banks and business owners.

When banks divert capital from this line of business or refuse new loans, it starts to put stress on the economy as a whole. The confidence of small business owners will take a hit. Employment hits a wall. This is how the recession materializes from what the stock market made up into a real concrete reality on Main Street.

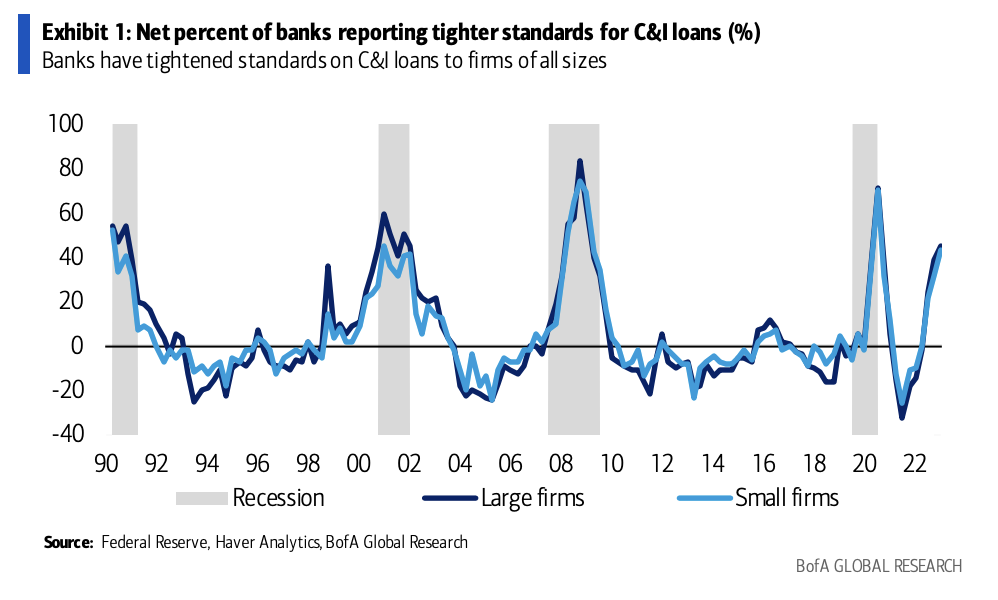

This morning, through Bank of America, here’s the net percentage of banks that are reducing C&I loans by tightening lending standards.

Historically, we see that the lending standards of large banks fluctuate up and down to match those of smaller banks. So if the shrinking of lending at smaller banks continues, the impact will be meaningful for everyone. We know the big banks are now benefiting from the local bank panic in terms of deposit movements, but that doesn’t mean they will attack lending growth. We are all on defense now. This is the very definition of a financial shock.

Last week’s FOMC decision to raise interest rates is going to look pretty ridiculous as the weeks and months go on. BofA economists point out what usually happens after shocks like the ones banks are currently enduring.

We use vector autoregression (VAR) on quarterly data from 1991 to 2022 to estimate the impact of changes in bank lending standards and terms on economic activity (21 March 2023 report Bank Estimation of downside risk from a sharp tightening of lending standards”). A 1-standard deviation shock to C&I loan lending standards and banks’ willingness to lend to consumers would reduce private consumption by a cumulative 1% to 2% over six quarters and employment by a cumulative 2% to 4% over six quarters. % has been found to decrease. Cumulative 10-15% reduction in structural and capex over 6-10 quarters and 15% reduction in underlying C&I loan growth over 10 quarters.

Tighter standards for consumer loans will result in a cumulative 10% decline in consumer loans over approximately 10 quarters. There is also a fairly short time lag between tightening lending standards and economic outcomes. Benefits tend to appear within about two to three quarters. Moreover, the shock to C&I and consumer loan lending standards is very persistent and, generally speaking, unabated. This is similar to previous findings that found that shocks to financial conditions can cause long-term declines in activity data…

SVB, Signature and Credit Suisse are not small banks. Regardless of what happens to depositors, their collective demise this month will be looked back on as the beginning of a hard landing. Whether a rate cut by the Federal Reserve later this year matters at this point I don’t know. It may be too late.

sauce:

Central banks continue to follow strategy, and so do we

Bank of America – March 24, 2023