Since the 1960s, the Capital Asset Pricing Model (CAPM) has become what investors and Christians are to the Bible. It is the unquestionable North Star to which everything else in the belief system is tied.

It has since been completely disproved (CAPM, not the Bible).

But the decades it has existed as the most sacred “law” of finance have made it deeply ingrained in the psyche of today’s investors. Unfortunately, this led them like lemmings falling off a cliff with high-risk stocks. idea Promised “expensive” expected return investment.

CAPM is a formula that attempts to determine an asset’s expected return based primarily on its volatility.

According to CAPM, there is a positive linear relationship between stock volatility and expected future returns. The higher the volatility of a stock, the higher the expected return in the future.

Many investors interpret this as follows.

Reduced to a rhyming maxim.

Of course, the shareholders of recently failed local banks don’t even have a piece of the biscuit to show the risks they’ve taken on. These stocks are certainly volatile. But a quick glance at the Regional Bank ETF (KRE) chart shows that this doesn’t bode well for future returns.

(Meanwhile, my stock valuation model warned of excessive risk a long time ago actual collapse. )

More on that later…

First, let’s look at CAPM and its “low volatility” factor that reveals the “higher risk = higher return” fallacy.

on the contrary…

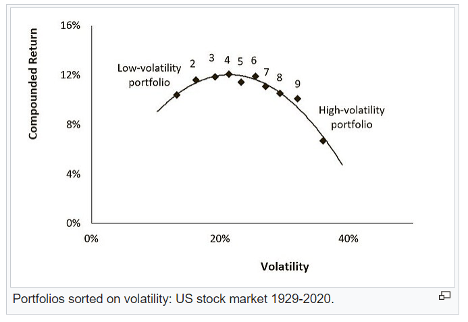

Dozens of academic research studies demonstrate that premium investors outperforming the market can earn by investing. low-volatility — not high volatility — equities.

Evidence for a low volatility premium goes back over 90 years, so this is definitely not a passing anomaly. The chart below shows compounded returns for low and high volatility portfolios from 1929 to 2020.

There are many explanations for the existence of this counterintuitive relationship between volatility and expected returns…

For one, most investors have proven to be averse to using leverage. Leverage is borrowing money to invest in positions larger than you have cash on hand.

Without that aversion, it would make sense for an investor to build a portfolio of low volatility stocks…and then leverage it conservatively to match the returns of a high volatility portfolio.

But “leverage” is a dirty word for most people. So instead, an investor looking for a higher return will forgo that option and simply invest in stocks. higher volatility.

This phenomenon is consistent with another behavioral bias, the ‘lottery’ effect.

Human nature urges us to seek “moonshot” returns in highly volatile stocks, even if the odds of getting such returns are very low and even lower than our estimates.

This bias tends to unduly inflate the prices and valuations of high volatility stocks while leaving low volatility stocks behind. Low price.

Taken together, investors show a preference for high volatility stocks, even though they have offered better returns for investors wise enough to pursue low volatility stocks.

Finally, high volatility stocks have far more mathematical hurdles to overcome than low volatility stocks.

This is a disproportionately large gain that must be amassed after the stock price falls.

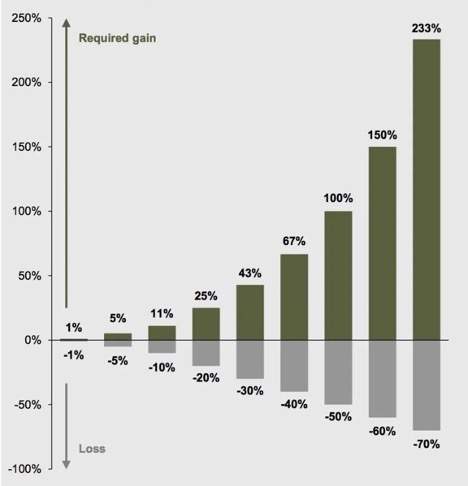

You’ve probably seen this chart before…

As you can see, when Disadvantage When volatility hits a highly volatile stock, you may need a very large rally just to get back to break even.

Stocks with lower volatility tend to hold up better in a downward cycle, making the path to recovery easier and allowing for more efficient compounding of capital over time.

my longtime member Fortune in the Green Zone In newsletters, I know that my team and I consider a stock’s volatility before recommending it. “Volatility” is one of the six factors my stock valuation model is built on.

We don’t always look for stocks with the lowest volatility, avoid shares with highest Volatility…because that is This factor is most effective in boosting overall returns.

Worth a try in many market environments Several additional volatility. So stocks in the middle of the pack in terms of volatility may actually be worth the risk, outperforming some of the lowest volatility stocks in the market.

But what you most definitely want to do is avoid the most volatile top 10% stocks.

Countless academic papers, as well as my own research and stock valuation models, show that this is the market’s most lagging and often negative Return value.

Today we are seeing very high volatility and that is what inspired me to write this essay. may be confused with

There is no better example than the ongoing woes of the local banking sector right now…

How to safely avoid a local bank failure

My lead analyst, Matt Clark, and I recently conducted a study to prove my experience with the volatility “sweet spot”…

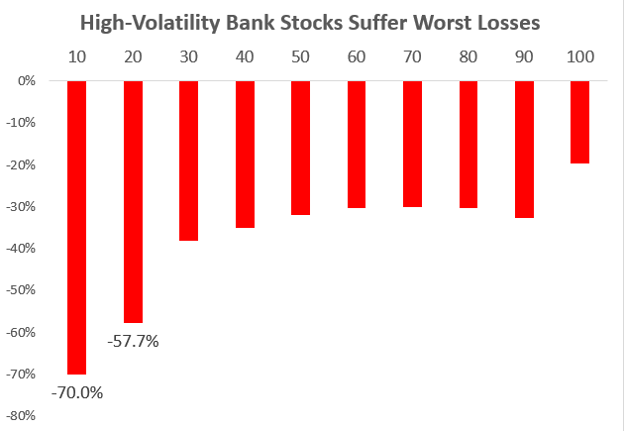

Create a list of individual stocks held in the SPDR S&P Regional Bank ETF (NYSE: KRE) and classify them into 10 “buckets” based on the volatility rating my stock valuation model assigns to each stock Did.

For clarity, We used model ratings as of March 6, 2023 … Monday Before The banking crisis began on Friday, March 10th at Silicon Valley banks.

Here are the average returns for each of the 10 buckets of local bank stocks through yesterday:

80% of bank stocks lowest Volatility is down 31% on average since March 6th. 20% of bank shares highest Volatility on average Twice i.e. -64%.

Additionally, who used my stock valuation model to avoid the 20% most volatile bank stocks Could have avoided all previous bank failures!

- Silicon Valley Bank (SIVB) triggered my model’s highest ‘high risk’ volatility threshold (top 10% most volatile) on October 24, 2022…the stock traded at $232. when It then dropped to $0.49, losing 99.8% of its value.

- Signature Bank (SBNY) was flagged as the top 10% most volatile stock when the stock traded at $132 on Nov. 21, 2022. A bank failure then sent the stock price down to his $0.09, leaving unsuspecting investors 99.9% of his losses.

- Pacific Western Bank (PACB) was flagged on December 12, 2022 with a share price of $24.83. As of yesterday, the stock has fallen more than 85% to $3.

- And failed bank First Republic Bank (FRC) crossed my model’s “high risk” volatility threshold on March 10…the day SIVB fell. FRC’s shares were trading at $31.21 at the time, but fell 99% to drop him below $0.50 before being seized by regulators and sold to JP Morgan.

We are eager to share this story of our unsung hero, the “low volatility” factor. Because so many investors simply don’t know it exists.

And seeing how that alone helped avert the worst regional banking crisis, the crisis I believe no It’s over — I feel I have to get the message across!

we all know that all Investing requires taking risks.but you don’t have to take Excessive Risk, or uncompensated risk…I think you have to, especially if you’re still chasing the most volatile stocks. “Take the risk…let’s get the biscuits.”

the plain fact is you please do not!

I showed today that a little volatility is a good thing.

If a stock moves little, you can’t expect it to have a significant impact on your wealth. If it moves too much…the needle may be feeding in the wrong direction.

My goal is to find a stock that moves the needle in the right direction. To that end, it is imperative to learn the disproven mantra of “high volatility, high returns”.

for good profit

Adam OdellEditor, 10x stock

Adam OdellEditor, 10x stock

PS Speaking of moving your “wealth needle” in the right direction…

I recently spoke with a publisher to extend the sale of access to my research advisory that beat the Russell 2000 10-1 from the start. 10x stock.

One reason is that due to increased market volatility, my recent $5 stock recommendations Even more fascinating…and I want anyone on the fence to learn more about them.

Another reason is… I couldn’t be more bullish on these ideas.

They are not the stocks that appear on the front page of CNBC or Yahoo Finance. But each of them is now an important part of robust, inflation-proof, and recession-proof portfolios.

The fact that you can participate in each for less than 1 fiber per share is just the icing on the cake.

Learn more about these stocks hereand how to participate.

What bothered me was the last $2.99 charge from Apple.

I spent months noticing my credit card bills getting higher and higher each month.

all It will take longer today.

But a lot of it was due to what I call “payment creep.”

Subscribe to this streaming service for $10 and other app services for $5. Neither seem like a lot of money.

But next thing you know, you’re paying hundreds of dollars extra. Most of them are unnecessary. And that last his $2.99 was a straw that broke a camel’s back.

I deleted tons of old files from iCloud and was able to cut $2.99 off my monthly bill. I checked my Microsoft subscriptions and it looks like I was paying over $40/month for the old OneDrive package. The new one is just $25 and comes with Office.

Chopped another bill!

I reviewed my cell phone bill. For reasons long forgotten by history, I was paying my wife an extra $10 a month for a phone line she hasn’t used in two years. gone!

I had a frilly Adobe Acrobat subscription that I never used. I downgraded from a $21 plan to a $14 plan.

I reviewed the magazines and newspapers I subscribe to. My rule of thumb: Any subscription that hasn’t been read in 6 months is retired. It ended up being hundreds of dollars back in my pocket.

And then there was the streaming service…

My entire family of five is addicted to Netflix, except for my 2-year-old daughter. never get rid of it.but until next season winning time I’m not paying HBO.

I canceled Disney Plus as well, but it might come back when the kids have summer vacation.I saved over $30 on two subscriptions.

My kids are always exhausted from too many extracurricular activities. Some of them seemed like great ideas a year before her, but now my kids have mostly lost interest and just watch them in action. We also see some savings from these costs.

I mention all this because I know I’m not the only one. Every dollar you and I deduct from your monthly service costs is a dollar that companies like Disney and Apple don’t make a profit.

When it comes to economics, it can be difficult to distinguish between cause and effect. It is often circular. Bonuses were less this year, so people cut back on spending…because people cut back on spending and companies benefited.

But that’s where we are today. Inflation causes people to reassess their spending, which comes from the (now curtailed) revenues of the companies that provide services.

This ends only when the appropriate recession clears the board.

My advice: When it comes to volatility in this market, especially when it comes to opportunities, consult Adam.

You really don’t want to miss out on his latest research. small capAs he said they are trading for under $5. But these are poised to skyrocket next year. If you’d like to learn more about Adam’s recommendations in this space, Visit here to get started.

nice to meet you,

Charles SizemoreEditor-in-chief, The Banyan Edge

Charles SizemoreEditor-in-chief, The Banyan Edge