Legend has it that Nero was playing the piano while Rome was burning. This legend is not true.

First of all, fiddles hadn’t been invented yet. And even if this legend is taken figuratively, most accounts say Nero was in Rome trying to save him from a fire.

This is the year 64 AD. The fire lasted him six days. It flattened nearly three-quarters of the city.

When investigating the damage, Nero decided to build a large palace on the ruins of part of the city. That’s one of the reasons why the fiddle legend is so ingrained in history.

When considering where to build a palace, it’s easy to think of the motives of fires as sinister. The truth is more complicated.

According to one theory, Nero cared about the citizens of Rome. He developed roads to ensure access to food. He built a covered market to ease the discomfort of the weather. He enforced stricter building codes after the fire.

These and other good deeds are not as memorable as the image of a tyrant fiddling with a musical instrument while watching the flames devour Rome. And the phrase “Nero was messing around while Rome burned” became a metaphor for inaction in times of crisis.

I mention this story because it helps illustrate how the Federal Reserve is coping with the current state of the economy…

The Fed is by no means inactive. But there are also many fires to extinguish. And when you spray the hose in one direction, the fire blazes in the other and gets out of control…

There are ways to improve the performance of your portfolio during this economic catastrophe, but many of you haven’t and still haven’t thought about it after reading this. But the rare few who do may be rewarded.

U.S. Economy Rebounds, Fed Watches

Fed Chairman Jerome Powell might be compared to Emperor Nero. He has done many things right. But the Fed’s decision to wait for more data before raising rates is concerning. This is because the danger of setting fire to the economy increases even further.

If prices rise even higher, many families will be left behind.

For example, the latest CPI report has lowered inflation to 4%, but food prices are still too high.household food costs have risen almost 20% 2 years. at the same time, Wages rose 4.3%.

No one wants to hear about the impact of the Fed’s policy delay when checking out at the grocery store. they want lower prices.

Grocery stores aren’t the only ones on fire. Since the pandemic, house prices have risen sharply.And this is not just a US problem, the International Monetary Fund believe Fifteen of the 38 developed economies they surveyed are at high risk of a housing crisis.

The Fed should help families fight inflation. But that requires high interest rates. And other powerful people don’t want high interest rates.

Low interest rates allowed Congress to pass a budget with trillions of dollars in deficit. As interest rates rise, the cost of borrowing increases. Even if funding costs increased by just 1% for him, government losses could exceed $300 billion for him.

Even with annual revenues of nearly $5 trillion, this is a huge amount.

But this is not just a national issue. Economies outside the US are struggling to sustain growth.We know a recession threatens US economic expansion

Germany (Europe’s largest economy) and the UK are no longer threatened by a recession. already in them. Emerging markets in Europe are expected to plunge into recession this year. And China’s growth is slowing.

The Fed should try to promote growth in the global economy. But to do that, we need to lower interest rates. Low interest rates boost business investment and create jobs. This is the formula for growth that central bankers have relied on for hundreds of years.

Of course, lower interest rates would make inflation even worse. This sums up the Fed’s problem.

Whatever Mr. Powell does, he faces problems. Your best course of action might just be to take out your violin and watch the flames from afar.

For us retail investors, this is no time to be lazy. In times of crisis, or, to use Nero’s words, when everything is on fire, there are many benefits.

The best thing we do as investors is to keep a close eye on short-term trading opportunities that arise during volatile times.that’s exactly what we do every morning trade room Five days a week, when the market is open.

One of our most popular strategies has outperformed the market by 33x over the past two months (April and May). And there is also a new one that I am designing and testing with the Trade Room community.

Click here to see what cutting-edge techniques we currently use to find new deals.

nice to meet you, Michael KerrEditor, exact profit

Michael KerrEditor, exact profit

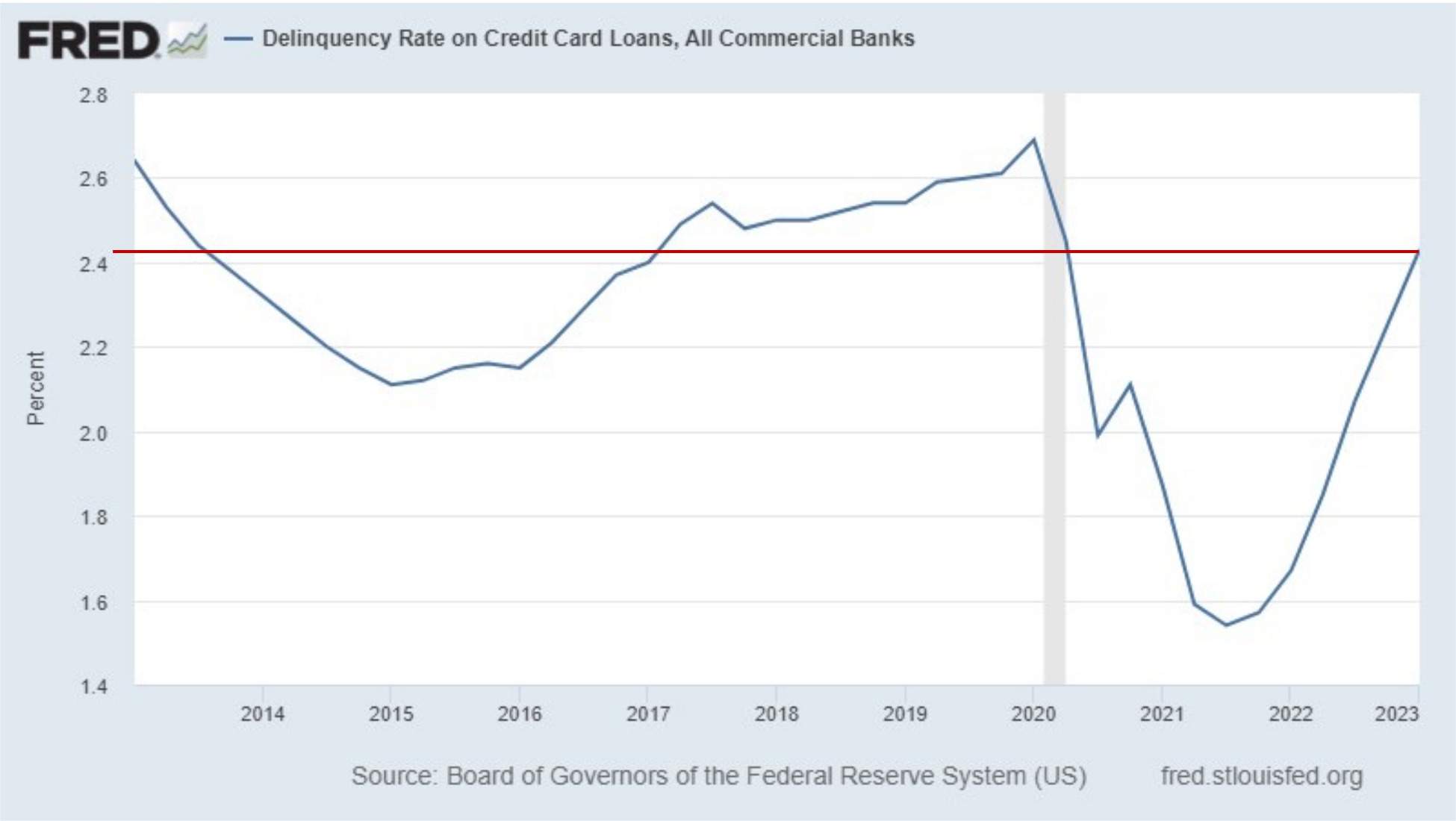

On Tuesday, I pointed out that US consumers are again avoiding credit cards. Total credit card debt is approaching $1 trillion for the first time.

Let’s take a closer look at these numbers.

Credit card delinquencies (over 30 days in arrears) follow the same basic pattern as credit card balances.

These delinquencies are at record lows in 2020 due to increased income from stimulus measures, student loan freezes and, in some cases, reduced credit obligations due to rent freezes. There was a general shortage of things to spend money on during the pandemic.

And all of this worked to reduce delinquencies. As my credit card balance increased, so did my late fees. Delinquency rates are now roughly in line with the average for the years before the pandemic.

why this is happening

We are swiping our cards more often as we try to make up for lost time on expensive experiences like vacations post-pandemic. I’m traveling to Europe with my kids for the first time in July and I’m already heartburned from seeing the expenses soar.

But there are also some more dangerous factors, such as high inflation. This forces us to spend more on regular basic necessities and pay less for government stimulus.

But here comes the problem.

Even if a recession doesn’t arrive soon, delinquency rates will skyrocket soon. many taller than.

The student loan moratorium, which has saved about 40 million Americans from high monthly payments over the past three years, will be lifted in two months. Millions of Americans will have to prioritize student loan payments over other debts such as credit cards.

Over the past few weeks, I have said that I expect a recession within the next three to six months. Will resuming student loan payments be a straw sandal to break a camel’s back?

I think it’s quite possible.

Mike Kerr believes that the best way to navigate the unknown in this market is to be agile in short-term trading. Take profit in and out, avoid the plunge and take advantage of the surge.

Want to learn more about Mike’s most popular (and successful) trading tactics? Go here to check out his trade room.

nice to meet you,

Charles SizemoreEditor-in-chief, The Banyan Edge

Charles SizemoreEditor-in-chief, The Banyan Edge