Note from Editor-in-Chief Charles Sizemore: This week, banyan edgeHere we feature insights from Matt Clark, Adam O’Dell’s right-hand analyst and Chief Research Analyst for Money & Markets.

Due to his past career as a journalist, Matt is well versed in the political events that affect our financial world. And last week, he became aware of an underreported statement by a key White House figure that could significantly reshape the banking system.

Learn what Matt uncovered and why it created a small local bank. One of the greatest short-term opportunities since 2008…

Treasury Secretary Janet Yellen made a casual remark a few weeks ago during a meeting with CEOs of big banks.

Former Fed Chairman said: More bank mergers may be needed to overcome the current crisis. (A merger is like… oh I don’t know… JP Morgan’s acquisition of First Republic a month ago).

The executives must have been big fans of this endorsement. JPMorgan CEO Jamie Dimon must be thrilled with the opportunity to get even more wealth for a penny in dollars and absorb it into America’s largest bank.

For smaller local banks and financiers, it was more like getting bad news from a doctor. The Treasury Secretary suggested that less competition, less choice and greater monopoly in the financial industry is the best path to stability.

Not surprisingly, traders punished smaller regional bank stocks. They’ve taken it for granted…but the report sent the SPDR S&P Regional Banking ETF (NYSE:KRE) down almost 2% on the day.

Any rational capitalist would agree that this trend does not benefit the everyday consumer. After all, competition is a hallmark of capitalism.

Still, there is no denying that this trend is real. The world’s most powerful governments now support big banks growing at the expense of smaller banks. It needs our attention.

There are many things you can do to make sure you take advantage of this trend. Now let’s talk about it…

Why bigger is better

Let’s quickly return to the financial crisis of 2008.

The big banks were at the center of the financial collapse as they favored risky lending practices, leading to the housing sector bubble that eventually burst.

Most of us remember how it went…

However, some good results came out of that, and they are what we are today. Specifically, the Dodd-Frank Act enacted by the government in 2008 left the big banks’ balance sheets much cleaner than they were then. Thanks to that, they are successfully coping with the current crisis.

Interestingly, we are now seeing the exact opposite of what happened in 2008. Small banks are now the problem.

They have significant exposure to long-term government bonds, as well as significant exposure to the risky commercial real estate market. The sector is currently facing a number of headwinds due to increased remote work and rising interest rates…despite little decline in demand for office space, refinancing deadlines are looming in the next two years.

The Treasury’s exposure behind the scenes, and even its exposure to commercial real estate, has had a devastating impact on smaller regional banks. This imbalance fuels the “bigger is better” trend.

All else being equal, the likelihood of a decline in trustworthy banks in the United States 10 years from now is significantly higher than an increase.

And two ways come to mind for investors to prepare for such scenarios:

Part 1: Focus on acquiring big banks. As I said earlier, the big banks are not in a great position to scale at the moment.

Take JP Morgan, for example. The company is the largest bank in the United States, with a market cap of over $400 billion and deposits of over $2.3 trillion.

Grandfather of the banking industry. But is it a good buy?

To answer that, let’s take a look at Adam’s own Green Zone Power Rating System…

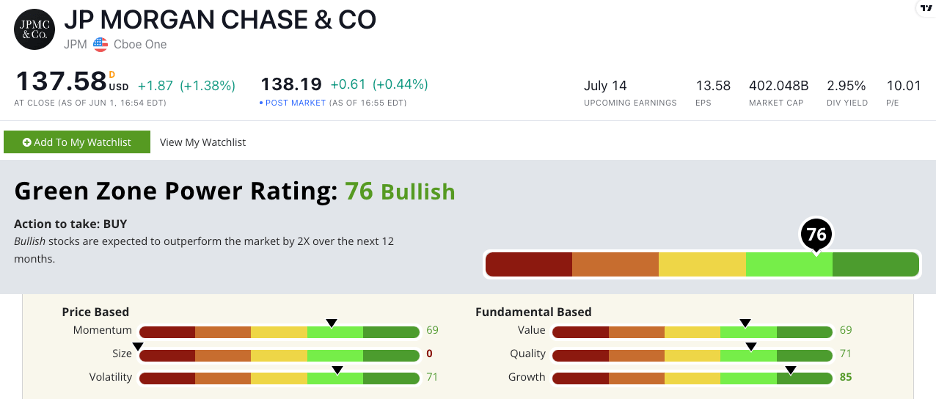

JPM green zone power rating In June 2023.

JPM stock has given only green light for every factor other than size, which is to be expected for a $400 billion behemoth.Nonetheless, stocks that rank so high are Trends to significantly outperform the market over the next 12 months.

JPM may be the best big bank stock you can buy today. But let’s say you don’t want to buy big bank stocks. I’m not going to blame you for that.you can do it are you OK With JPM stock… but it may be years before you see a big return.

Here are some more short-term ideas.Both Adam and I believe we can bring 100%, 200% and even more benefits. MonthNot in a few years, but in the future…

Part 2: Shorting local bank stocks. The $8 billion profitable position held by hedge funds since the banking crisis began is no lie. At this point, local bank stocks are a toxic asset to own.

Once again, the Green Zone Power Rating System allows us to properly assess its quality. My model doesn’t track exchange-traded funds, but I can look at some of the top holdings in the SPDR S&P Regional Banking ETF (NYSE: KRE) to spot weaknesses.

Four of KRE’s top five holdings are: 36 or less About Adam’s rating system. At best, these stocks are expected to underperform the market over the next 12 months.

That means, just like the hedge funds that have liquidated in the last few months, trading with hedge funds can be hugely profitable.

To be clear, I don’t recommend shorting stocks on Money & Markets unless you’re the type to dabble in hedge fund traders. If the maximum profit is 100% for him even if the stock goes to zero and the potential risk is infinite, the ratio is totally unreliable for the everyday small investor.

However, we recommend This method is detailed here by Adam O’Dell.

This is a way to profit from the continued decline in local bank stocks without the risks associated with short selling.

Buy one specific ticker in your brokerage account and sell it when you reach your profit target. Simple like that.

again, this linkAdam presents four financial stocks he believes could be the “next stock to lose” in the ongoing banking crisis.

If you have deposits, loans, or retirement assets with any of these four banks, we strongly encourage you to consider your relationship with them. And if you own stock, it’s easy to sell today.

The prospect of less competition and more monopolies in the financial sector is frightening. However, it is the road that is laid out before us.

In times of great upheaval like the one we live in, it’s important to ignore the noise and speculation and find ways to turn the tide in your favor.

Currently, we have acquired a large high-quality bank, short a small, low-quality bank It’s the move you should do. Until that changes, I recommend doing just that.

secure transactions,

Matt Clark, Chief Research Analyst, Money & Markets